Q: 11

Maria Harris is a CFA® Level 3 candidate and portfolio manager for Islandwide Hedge Fund. Harris is

commonly involved in complex trading strategies on behalf of Islandwide and maintains a significant

relationship with Quadrangle Brokers, which provides portfolio analysis tools to Harris. Recent

market volatility has led Islandwide to incur record-high trading volume and commissions with

Quadrangle for the quarter. In appreciation of Islandwide's business, Quadrangle offers Harris an all-

expenses-paid week of golf at Pebble Beach for her and her husband. Harris discloses the offer to her

supervisor and compliance officer and, based on their approval, accepts the trip.

Harris has lunch that day with

Options

Discussion

No comments yet. Be the first to comment.

Be respectful. No spam.

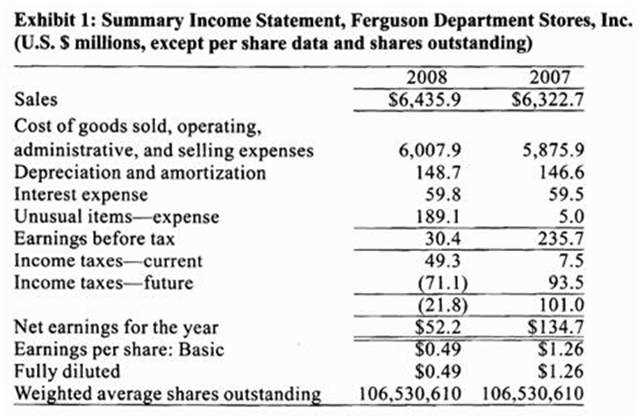

In 2008, FDS also reported an unusual expense of $189.1 million related to restructuring costs and

asset write downs.

In 2008, FDS also reported an unusual expense of $189.1 million related to restructuring costs and

asset write downs.

In response to questions from a colleague, Emery makes the following statements regarding the

merits of earnings yield compared to the P/E ratio:

Statement 1: For ranking purposes, earnings yield may be useful whenever earnings are either

negative or close to zero.

Statement 2: A high E/P implies the security is overpriced.

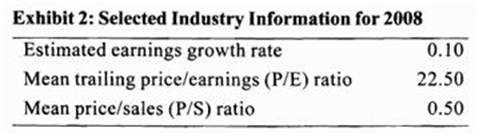

According to FDS's price-to-sales ratio for 2008, based on the post-expansion announcement stock

price, FDS is:

In response to questions from a colleague, Emery makes the following statements regarding the

merits of earnings yield compared to the P/E ratio:

Statement 1: For ranking purposes, earnings yield may be useful whenever earnings are either

negative or close to zero.

Statement 2: A high E/P implies the security is overpriced.

According to FDS's price-to-sales ratio for 2008, based on the post-expansion announcement stock

price, FDS is: 2. The Neoclassical Growth Era o/Alphia (1951-1990)

During the neoclassical growth period, Alphia experienced a period of great economic growth. For

example, from 1986 to 1990, Alphia's capital per hour of labor grew at a 9% annual rate, while real

GDP grew at 7% per annum.

Also, Alphia was able to achieve economic growth rates and income levels comparable with many of

its neighboring countries during the neoclassical growth period. Alphian scientists, together with the

engineering department of the University of Ullom, provided access to the finest technology in the

world. In addition, Alphia opened up its equity markets to outside investors and allowed its currency

to float. Dr. Satish believes that, given time, these capital market improvements should allow the

Alphian economy to achieve an economic growth rate and per capita income level comparable to any

country in the world.

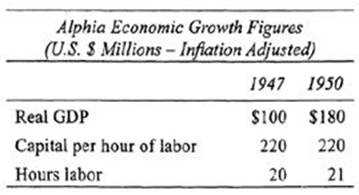

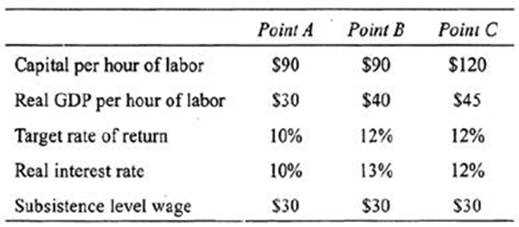

To understand the role of technology in the growth of the Alphian economy (using neoclassical

growth theory assumptions), the following table was developed to show the increased productivity

of Alphian farmers using disease resistant grains. Assume new disease resistant grain technology was

introduced into the Alphian farm economy at Point A.

2. The Neoclassical Growth Era o/Alphia (1951-1990)

During the neoclassical growth period, Alphia experienced a period of great economic growth. For

example, from 1986 to 1990, Alphia's capital per hour of labor grew at a 9% annual rate, while real

GDP grew at 7% per annum.

Also, Alphia was able to achieve economic growth rates and income levels comparable with many of

its neighboring countries during the neoclassical growth period. Alphian scientists, together with the

engineering department of the University of Ullom, provided access to the finest technology in the

world. In addition, Alphia opened up its equity markets to outside investors and allowed its currency

to float. Dr. Satish believes that, given time, these capital market improvements should allow the

Alphian economy to achieve an economic growth rate and per capita income level comparable to any

country in the world.

To understand the role of technology in the growth of the Alphian economy (using neoclassical

growth theory assumptions), the following table was developed to show the increased productivity

of Alphian farmers using disease resistant grains. Assume new disease resistant grain technology was

introduced into the Alphian farm economy at Point A.

3. The New Growth Era (1991-Today)

Since the Alphian energy crises of the late 1980s, the economy has been in transition. The AEDA goal

is to have more than 50% of Alphian GDP coming from what we now call knowledge capital based

industries by the year 2020. Given the large and growing population and their constant need for

health care, the pharmaceutical industry was Alphia's first knowledge capital based industry. Dr.

Satish believes that a focus on knowledge capital will enhance the long term growth prospects of

Alphia's economy.

According to the classical growth theory, Alphia would:

3. The New Growth Era (1991-Today)

Since the Alphian energy crises of the late 1980s, the economy has been in transition. The AEDA goal

is to have more than 50% of Alphian GDP coming from what we now call knowledge capital based

industries by the year 2020. Given the large and growing population and their constant need for

health care, the pharmaceutical industry was Alphia's first knowledge capital based industry. Dr.

Satish believes that a focus on knowledge capital will enhance the long term growth prospects of

Alphia's economy.

According to the classical growth theory, Alphia would: Smith has discovered that WMC has a small subsidiary in Ukraine. The Subsidiary follows IAS

accounting rules and uses FIFO inventory accounting. The Ukrainian subsidiary was acquired ten

years ago and has been fully integrated into WMC's operations. WMC obtains funding for the

subsidiary whenever the company finds profitable investments within Ukraine or surrounding

countries. According to forecasts from economists, the Ukrainian currency is expected to depreciate

relative to the U.S. dollar over the next few years. Local currency prices are forecasted to remain

stable, however.

One of the managers at WMC asks Smith to analyze a third subsidiary located in India. The manager

has explained that real interest rates in India over the last three years have been 2.00%, 2.50%, and

3.00%, respectively, while nominal interest rates have been 34.64%, 29.15%, and 25.66%,

respectively. Smith requests more time to analyze the Indian subsidiary.

Which of the following statements regarding the consolidation of WMC's Ukrainian subsidiary for the

next year is least likely correct? As compared to the temporal method, the Ukrainian subsidiary's

translated:

Smith has discovered that WMC has a small subsidiary in Ukraine. The Subsidiary follows IAS

accounting rules and uses FIFO inventory accounting. The Ukrainian subsidiary was acquired ten

years ago and has been fully integrated into WMC's operations. WMC obtains funding for the

subsidiary whenever the company finds profitable investments within Ukraine or surrounding

countries. According to forecasts from economists, the Ukrainian currency is expected to depreciate

relative to the U.S. dollar over the next few years. Local currency prices are forecasted to remain

stable, however.

One of the managers at WMC asks Smith to analyze a third subsidiary located in India. The manager

has explained that real interest rates in India over the last three years have been 2.00%, 2.50%, and

3.00%, respectively, while nominal interest rates have been 34.64%, 29.15%, and 25.66%,

respectively. Smith requests more time to analyze the Indian subsidiary.

Which of the following statements regarding the consolidation of WMC's Ukrainian subsidiary for the

next year is least likely correct? As compared to the temporal method, the Ukrainian subsidiary's

translated: Which of the following best describes the regulation being considered by the Wakullian government

for the electrical utility industry?

Which of the following best describes the regulation being considered by the Wakullian government

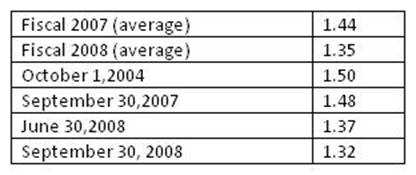

for the electrical utility industry? Other information to be considered • Exchange rates (CAD/USD)

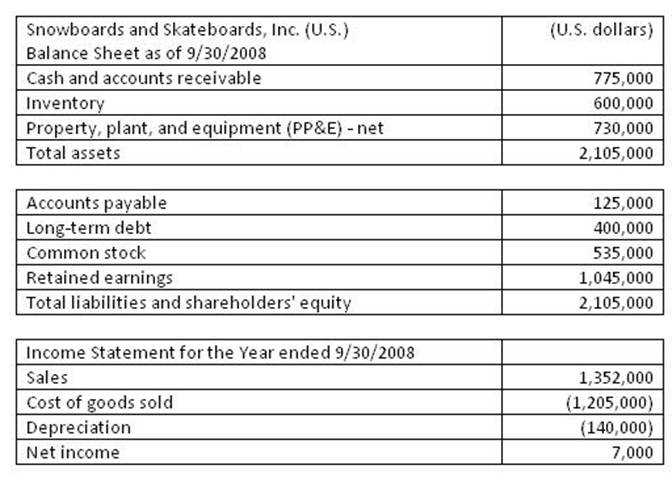

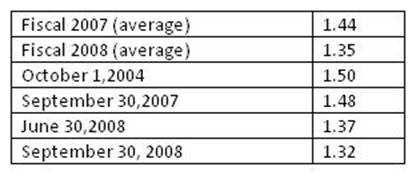

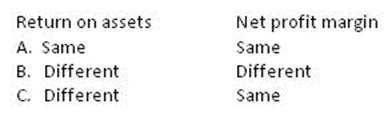

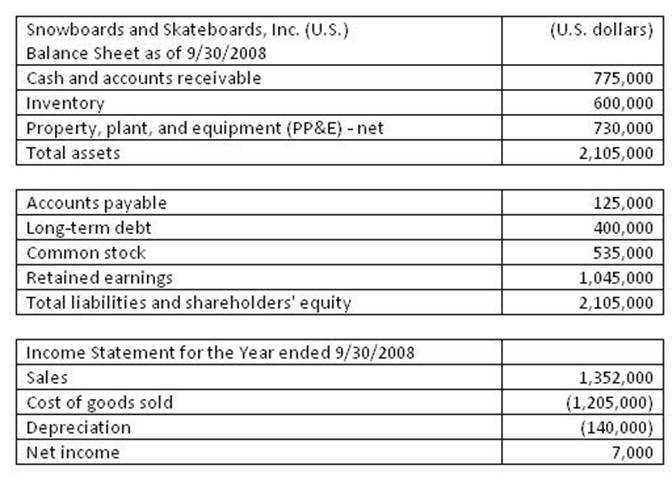

Other information to be considered • Exchange rates (CAD/USD)  • Beginning inventory for fiscal 2008 had been purchased evenly throughout fiscal 2007. The company uses the FIFO inventory value method. • Dividends of USD 25,000 were paid to the shareholders on June 30, 2008. • All of the remaining inventory at the end of fiscal 2008 was purchased evenly throughout fiscal 2008. • All of the PP&E was purchased, and all of the common equity was issued at the inception of the company on October 1, 2004. No new PP&E has been acquired, and no additional common stock has been issued since then. However, they plan to purchase new PP&E starting in fiscal 2009. • The beginning retained earnings balance for fiscal 2008 was CAD 1,550,000. • The accounts payable on the fiscal 2008 balance sheet were all incurred on June 30, 2008. • The U.S. subsidiary's operations are highly integrated with the main operations in Canada. • The remeasured inventory for 2008 using the temporal method is CAD 810,000. • All monetary asset and liability balances are the same as they were at the end of the 2007 fiscal year, except that long-term debt was USD 467,700. • Costs of goods sold under the temporal method in 2008 is CAD 1,667,250. Suppose the parent uses the all-current method to translate the subsidiary for fiscal 2008. Will return on assets and net profit margin in U.S. dollars before translation be the same as, or different than, the translated Canadian dollar ratios?

• Beginning inventory for fiscal 2008 had been purchased evenly throughout fiscal 2007. The company uses the FIFO inventory value method. • Dividends of USD 25,000 were paid to the shareholders on June 30, 2008. • All of the remaining inventory at the end of fiscal 2008 was purchased evenly throughout fiscal 2008. • All of the PP&E was purchased, and all of the common equity was issued at the inception of the company on October 1, 2004. No new PP&E has been acquired, and no additional common stock has been issued since then. However, they plan to purchase new PP&E starting in fiscal 2009. • The beginning retained earnings balance for fiscal 2008 was CAD 1,550,000. • The accounts payable on the fiscal 2008 balance sheet were all incurred on June 30, 2008. • The U.S. subsidiary's operations are highly integrated with the main operations in Canada. • The remeasured inventory for 2008 using the temporal method is CAD 810,000. • All monetary asset and liability balances are the same as they were at the end of the 2007 fiscal year, except that long-term debt was USD 467,700. • Costs of goods sold under the temporal method in 2008 is CAD 1,667,250. Suppose the parent uses the all-current method to translate the subsidiary for fiscal 2008. Will return on assets and net profit margin in U.S. dollars before translation be the same as, or different than, the translated Canadian dollar ratios?

Other information to be considered • Exchange rates (CAD/USD)

Other information to be considered • Exchange rates (CAD/USD)  • Beginning inventory for fiscal 2008 had been purchased evenly throughout fiscal 2007. The company uses the FIFO inventory value method. • Dividends of USD 25,000 were paid to the shareholders on June 30, 2008. • All of the remaining inventory at the end of fiscal 2008 was purchased evenly throughout fiscal 2008. • All of the PP&E was purchased, and all of the common equity was issued at the inception of the company on October 1, 2004. No new PP&E has been acquired, and no additional common stock has been issued since then. However, they plan to purchase new PP&E starting in fiscal 2009. • The beginning retained earnings balance for fiscal 2008 was CAD 1,550,000. • The accounts payable on the fiscal 2008 balance sheet were all incurred on June 30, 2008. • The U.S. subsidiary's operations are highly integrated with the main operations in Canada. • The remeasured inventory for 2008 using the temporal method is CAD 810,000. • All monetary asset and liability balances are the same as they were at the end of the 2007 fiscal year, except that long-term debt was USD 467,700. • Costs of goods sold under the temporal method in 2008 is CAD 1,667,250. Are Hally's statements regarding foreign currency translation correct?

• Beginning inventory for fiscal 2008 had been purchased evenly throughout fiscal 2007. The company uses the FIFO inventory value method. • Dividends of USD 25,000 were paid to the shareholders on June 30, 2008. • All of the remaining inventory at the end of fiscal 2008 was purchased evenly throughout fiscal 2008. • All of the PP&E was purchased, and all of the common equity was issued at the inception of the company on October 1, 2004. No new PP&E has been acquired, and no additional common stock has been issued since then. However, they plan to purchase new PP&E starting in fiscal 2009. • The beginning retained earnings balance for fiscal 2008 was CAD 1,550,000. • The accounts payable on the fiscal 2008 balance sheet were all incurred on June 30, 2008. • The U.S. subsidiary's operations are highly integrated with the main operations in Canada. • The remeasured inventory for 2008 using the temporal method is CAD 810,000. • All monetary asset and liability balances are the same as they were at the end of the 2007 fiscal year, except that long-term debt was USD 467,700. • Costs of goods sold under the temporal method in 2008 is CAD 1,667,250. Are Hally's statements regarding foreign currency translation correct?