Q: 15

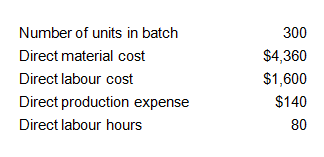

CORRECT TEXT Refer to the Exhibit.  A company operates a batch costing system. Production overhead costs are absorbed into the cost of batches using a direct labour hour rate. Other overhead costs are absorbed at a rate of 20% of total production cost. The company adds a mark-up of 10% to total cost in order to derive its selling prices. Budgeted production overheads for the period are $44,000 and the budgeted level of activity is 8,800 direct labour hours. The following data are available for batch number 309: The required selling price per unit (to two decimal places) is:

A company operates a batch costing system. Production overhead costs are absorbed into the cost of batches using a direct labour hour rate. Other overhead costs are absorbed at a rate of 20% of total production cost. The company adds a mark-up of 10% to total cost in order to derive its selling prices. Budgeted production overheads for the period are $44,000 and the budgeted level of activity is 8,800 direct labour hours. The following data are available for batch number 309: The required selling price per unit (to two decimal places) is:

Your Answer

Discussion

No comments yet. Be the first to comment.

Be respectful. No spam.